Business travel and events costs to rise through 2024: CWT

Global business travel and events costs are set to climb higher through the remainder of 2023 and into 2024, albeit at a much more moderate pace than the exceptionally steep increases seen in 2022.

This is according to the 2024 Global Business Travel Forecast, published today by CWT and the Global Business Travel Association (GBTA), the world’s largest business travel trade organisation.

Rising fuel prices, labour shortages, and supply chain challenges, coupled with red hot demand, caused travel prices to skyrocket in 2022 – far surpassing some of the increases outlined in last year’s forecast.

Lingering economic uncertainty and a gradual easing of supply-side constraints are expected to result in more subdued price increases over the next 12-18 months, according to the report, which uses anonymised data generated by CWT and GBTA, with publicly available industry information, and econometric and statistical modelling developed by the Avrio Institute.

“A potent combination of demand and supply-side pressures propelled travel prices higher than expected last year,” said Patrick Andersen, CWT’s CEO.

“Looking forward, prices seem to be levelling off with much milder increases projected over the next 12 to 18 months. We could now be looking at the true new cost of travel. Our focus remains on helping our customers find the right strategies and solutions to get the most out of their travel budgets, meet their ESG commitments, and maximize the ROI on their travel spend.”

“As this research outlines, it’s clear that rising costs and pricing pressures will likely continue to be a significant factor in business travel for the foreseeable future. And as we experienced over the past few years, we may also continue to see different pricing fluctuations across industry verticals, business sectors and global regions. While business travel continues to rebound, there will be a continuing balancing act among demand, cost, and ESG concerns. So, with a forecast ahead for more volatility, our goal is to provide insights like these to help travel buyers, suppliers, intermediaries and finance executives continue to understand, evaluate and adjust their business travel strategies,” said Suzanne Neufang, Chief Executive Officer, GBTA.

Air

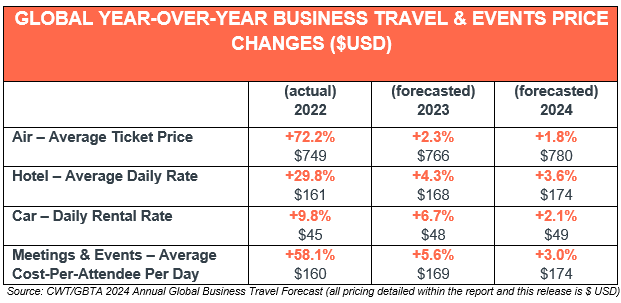

The global average ticket price (ATP) of flights booked for business travel rose dramatically in 2022, experiencing record price increases. The ATP rose by 72.2 per cent YoY to $749 in 2022, far surpassing 2019 levels ($670).

While demand has recovered strongly with passenger numbers quickly approaching pre-pandemic levels, driven primarily by pent-up leisure travel demand, airline capacity continues to be constrained by labour shortages and supply chain issues. Looking forward, ATP growth is likely to be more modest at 2.3 per cent in 2023 and 1.8 per cent in 2024, albeit from an already high base. Still, many corporate buyers now have less leverage to negotiate with airlines, as their travel volumes remain below pre-pandemic levels.

However, in terms of year-over-year growth, the ATP in Asia Pacific climbed 148.7 per cent YoY in 2022 to $567 – the biggest increase seen in any region, despite a lack of international travel demand from China. Key business travel destinations, including Australia and Japan, fully reopened to vaccinated travellers and resumed visa exemption arrangements. Average airfares rose 75.3 per cent for Australia and 79.3 per cent for Japan in 2022, with a sharp rise in the share of long-haul tickets. As airlines in the region – particularly the major carriers from China – continue to add more international route capacity, the increased supply should help ease price pressures in the region, with ATPs forecast to rise 4.8 per cent in 2023 and 2.7 per cent in 2024.

Hotel

Like air travel ATPs, the global average daily rate (ADR) for hotel bookings exceeded earlier predictions, rising 29.8 per cent YoY to $161 in 2022. Occupancy rates have been high, but so have labour, energy, and food and beverage costs. In fact, several cities across the globe including London, Miami, and Singapore, reported their highest ADRs on record in 2022. Meanwhile, hotel construction remains down from its pre-pandemic peak, creating supply constraints. With fewer properties to compete against, existing hotels can sustain their pricing power for longer, even though ADR gains are slowing. ADRs are projected to climb a further 4.3 per cent in 2023 to $168, followed by a 3.6 per cent increase to $174 in 2024.

Ground transportation

Car rental supply has been constricted as companies sold vehicles during the pandemic when demand collapsed. As business returned, vehicles were not replaced at pace due to supply chain issues, largely due to a worldwide shortage of vehicle semiconductors which led to inflated vehicle prices. These factors have contributed to prices rising by 9.8 per cent YoY in 2022, with a further 6.7 per cent increase forecast this year. Pricing growth is expected to cool to 2.1 per cent in 2024.

Meetings and events

In-person meetings and events have rebounded more robustly than many had expected. Client acquisition and relationship building are key business goals that are not easily executed virtually. There has also been exceptionally strong demand for incentive trips, as companies seek to motivate and reward employees. In fact, CWT Meetings & Events has observed these trips becoming longer and more frequent and expects the trend to continue.

The average daily cost per attendee was $160 in 2022. This is expected to increase to $169 in 2023 and then $174 in 2024.

Lead times for events remain short in this post-pandemic world. However, organizers should now look at 2024 with a 12-month planning cycle if they want to keep prices at a reasonable level. At the same time, consolidating transient travel and M&E spend can give buyers more leverage when it comes to negotiating pricing.

Email the Travel Weekly team at traveldesk@travelweekly.com.au

2024 Global Business Travel Forecast cwt GBTA global business travel associationLatest News

Low-cost Indian carrier SpiceJet continues to burn cash

It’s not just low-cost Australian carriers that are facing hardship. SpiceJet, India’s version of Bonza, recently announced a 72 per cent reduction in its net loss versus last year. But, despite this improvement, the airline has posted losses for six straight years. But it has secured board approval to raise up to INR 30 billion […]

SAKA Museum recognised in TIME magazine’s World’s Greatest Places 2024

AYANA Resort Bali’s newly-opened cultural and events centre, SAKA Museum has been recognised in TIME magazine’s World’s Greatest Places list for 2024. Part of AYANA Bali’s resort destination, the museum integrates Bali’s rich history with state-of-the-art facilities, making it the centrepiece for the island’s spiritual and cultural heritage. TIME magazine’s inclusion of SAKA Museum in […]

Journey Beyond launches first brand-led campaign during Paris Olympics

Journey Beyond is pushing the boundaries. On The Ghan, you can't even see them!

Ascott Australia partners with Hotels for Trees

Hoteliers can take a 'Lyf' out of this book and improve their green credentials.

Victoria’s TAC Top Tourism Town Award winners for 2024

Keep looking in our own backyard. There are plenty of places to go.

Uniworld partners with Camilla Franks with Egyptian-inspired collection

We are in de-Nile about making puns combining Crocs and leopard prints, given this luxe partnership.

Aussies at Paris Olympics anxious about travel risks, with incidents already recorded

Fortunately one of our biggest gold medal hopes still held onto his pedals.

Banyan Tree Seaview Villas elevates Laguna Lang Co

If you've ever played golf in the tropics, start early. LIke way early. It's hot! Damn hot.

Silversea taps Barbara Biffi as senior vice president for global sales

Ultra-luxury and expedition cruise travel brand, Silverseas, has announced Barbara Biffi as its new senior vice president of global sales. Biffi joined the company in 2007, holding numerous positions and gaining a deep understanding of the brand, the preferences of its guests and its strategic goals, the company said. An Italian national with a wealth […]

Wendy Wu unveils new Japan travel brochure and itineraries

Get outta town! Off-beat Japan will be a lot less congested we figure than the usual tourist hotspots.

UK and Europe event organisers look to venues with sustainability integrity, ICC Sydney survey finds

Here in Sydney, you can even eat the table centrepieces. Although we advise they be cooked first.

Renos Rologas new general manager ANZ for FCM Travel

Two decades in the travel game! Let's hope Renos is in for the long haul at FCM.

Untamed Escapes to offer Cultural Day Tour from Port Lincoln in partnership with Maba Idi

International visitors travel thousands of kilometres for this experience. Time to share.

Luxe Finish Line Penthouses offer the best vantage point for the finish of the Sydney-Hobart

Long have we been following the yachts leavings Sydney Harbour and one day, we will see the finish, from this place!

In a busy world, proximity to nature is the new luxury

Forget Raffles, treat your nearest and dearest to a stay at the local campsite. They'll be super close to nature.

Circular Quay welcomes new Korean dining experience to Sydney Place

We once took Korean-American chef David Chang around Koreatown, Eastwood. Not happy about driving rain, loved the food.

MSC Cruises unveils a new outdoor kid-friendly attraction on World America

Drop your kid down the jaws of a shark and they come out 11 decks below. Sounds good to me.

Amadeus welcomes FCM Travel as new reseller partner of Cytric Easy

Cytric Easy, the travel management tool embedded in Microsoft Teams, is to be integrated into FCM Travel portfolio. Amadeus and FCM Travel have extended their Cytric distribution agreement to include Cytric Easy. With this new agreement, global travel management company FCM Travel, becomes a reseller of the innovative travel management collaboration solution embedded into Microsoft […]

Australian travellers abandon peer-to-peer stays and gravitate back to big hotels, survey finds

Doom scrolling Airbnb for the best-possible stay options two days out from departure was wearing us down, apparently.

Quark Expeditions launches the Ultimate Summer in the Arctic sweepstakes for travel advisors

Summer in the Arctic still means it's freezing. But hopefully a winning sweepstakes tickets will warm your cockles.

‘I bet it smells weird’ – Internet divided over floating restaurant in China

I you are still feeling peckish at the end of your meal, their fish tank is full. But can you eat koi?

‘Turn up in the Northern Territory this Spring’ campaign deals

Agents and airlines get all hot and sweaty over these enticing deals. Or did someone just turn the air-conditioning up?

‘Like nothing on earth’: Saudi Arabia’s new Treyam resort set in a Star Wars-style landscape

As long as Jar Jar Binks is not there, we would like a seat at the Mos Eisley Cantina please.

Raffles Hotels and Resorts is set to open in Tokyo in 2028

Time to get your vision boards at the ready! Raffles is landing in Tokyo!

‘A true honour’ – Andrew Stark wins Flight Centre Director’s Award for the second time

Congratulations Andrew! If you're a fan of British reality TV you might notice a familiar face.

Club Med debuts travel agent portal 2.0 with bonus prize for tops sales

See those people by the pool. That could be you. Start selling through the portal people!

Envoyage announces 2024 Australian Icons and rewards event in the Maldives

We were going to edit our name into the list but we chickened out.

HIF Global signs collaboration agreement with Airbus on eFuels

We know it's a good thing but can a jet fuel geek out there send in a diagram explaining this please.

Crystal announces release dates for 2026 itineraries

If you have started collecting 2026 itineraries then here is another one for you.

Cairns Airport unveils display of support for FNQ youth

If you were craving some winter sun now you have a cultural reason for booking a flight to Cairns.

Viking announces six new cruise itineraries

Now's the time to start learning Putonghua, Nihongo and Lhasa. Or maybe even know where these are spoken.

Join Qatar Airways, Celebrity Cruises & Klook – Showcase Your Brand at Click Frenzy Travel August 2024!

Clicking calmly will also be welcome when it comes to this particular deal. Click calmly here to find out more.

InsideAsia Tours launches new incentive that doubles agent commission

Double commission! We like the sound of that. Hope their system doesn't crash as a result.

Push to revive Parramatta’s iconic Roxy Theatre into entertainment destination

Long have we wished for this iconic heritage cinema to be revived as a tourist destination. Still waiting.

Qatar Airways signs an expansion to Boeing 777-9 aircraft order

Known as a quiet rural town in England, the entire global aviation industry now has its eyes on Farnborough.

Flight Centre shares down following revised profit guidance

The stock market moves fast. What will the rest of the week hold for Flight Centre?